Latest News

- Kerry Electronics (Zhucheng) Co., Ltd. successfully held the signing ceremony for academician workstations

- Song Hongwu, Deputy Mayor of Science and Technology Talents of Zhucheng City, and his entourage came to Kerry Electronics to visit and exchange

- 2021 ranking of the world's 100 largest defense companies, 7 Chinese companies on the list

- What will China's naval and air force equipment look like by 2030?

- Win the 6th round in July! Chang'erding successfully launched tianhua-1 04

- The monthly sales data of the first and second quarters reached new highs, and the operating performance improved significantly

- "Two bombs and one satellite": missiles, atomic bombs, man-made earth satellites | Great spirit creates greatness

- Research on three frontier science and technology industries: artificial intelligence, blockchain, and commercial aerospace in the next ten years

- Employee registration form download

Research on three frontier science and technology industries: artificial intelligence, blockchain, and commercial aerospace in the next ten years

Author:admin Time:2021-08-03 02:52:47

1. Artificial Intelligence 2030: The development of algorithms and computing power will reshape the automotive, medical, and entertainment industries

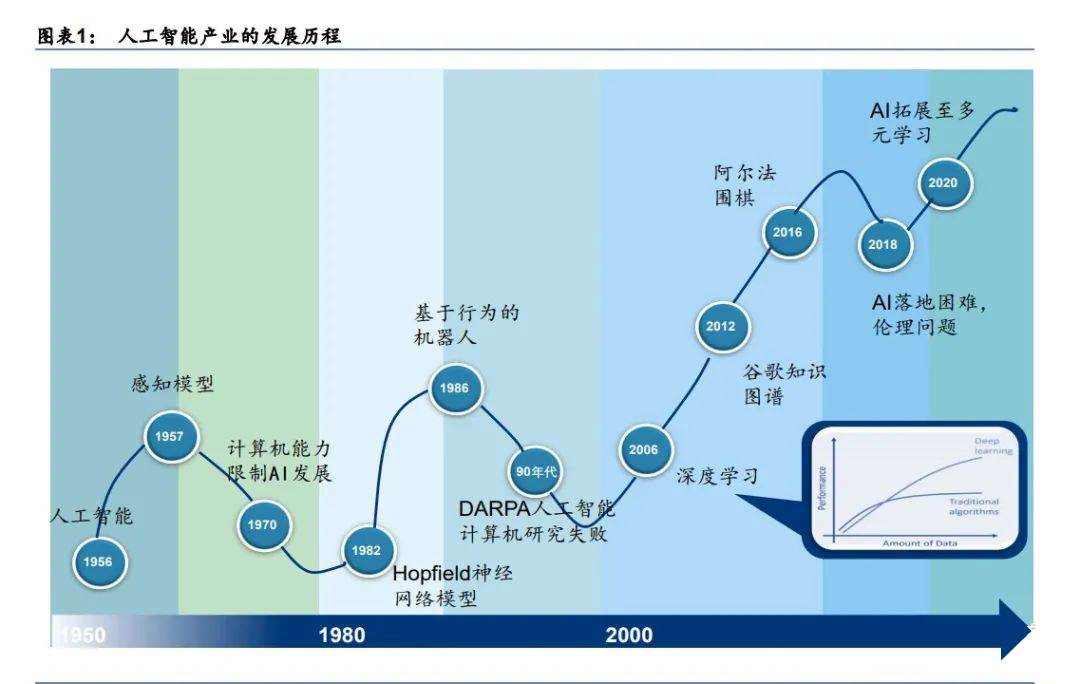

In the past ten years, the AI ??industry has ushered in the third wave in history, and it is also the fastest wave of development in more than 70 years. Based on deep learning theory, AI, driven by data, has reached or even surpassed human accuracy in specific fields such as face recognition and text translation, and it also has an efficiency far beyond that of humans. Chip manufacturing process upgrades and the development of foundry models have also enabled AI under big data to land. At the same time, AI is also opening the curtain in the field of software and hardware after changing the Internet ecology, and has begun to reshape areas such as security. The AlphaGo human-machine game also helps popularize the concept of AI. In summary, with the introduction of deep learning algorithms, breakthroughs in the semiconductor industry, and successful content promotion, AI has developed by leaps and bounds in the past ten years from professional technical theories, industrialization, and public awareness.

Investment and financing: AI companies gradually land in the capital market

In the primary market, the scale of global AI-related private equity financing continues to increase. The total investment in 2020 is 67.9 billion U.S. dollars, a year-on-year increase of 40%. With the development of the industry, investment has become more concentrated, forming a clear head effect. According to CCID consultants' statistics, in China's AI investment, the proportion of angel round AI investment dropped from 67% in 2016 to 34% in 2019.

After years of development, AI's business model has gradually become clear, and AI has also been favored by investors. From extensive investment to more focus on several major scenarios, applications have gradually shrunk to machine vision (CV), natural language processing (NLP), and AI platforms. , AI chips and other fields.

With the wider recognition of AI, the AI ??industry has ushered in a wave of entrepreneurship. Unicorn companies continue to emerge in the capital market and their valuations continue to increase. In 2020, the listing of AI companies has even begun. Companies such as Palantir, Tuya Smart, Schrodinger, C3.AI, and UIPath have successfully listed, and a large number of companies are lining up for listing. We judge that the market value of A/H/US stock AI companies will increase significantly in the future. my country's AI industry is showing a relatively high degree of prosperity. Megvii, Yitu and Yuncong among the four AI dragons in my country have all submitted prospectuses, and a large number of industries in the listed companies are also undergoing continuous transformation and upgrading under the AI ??wave.

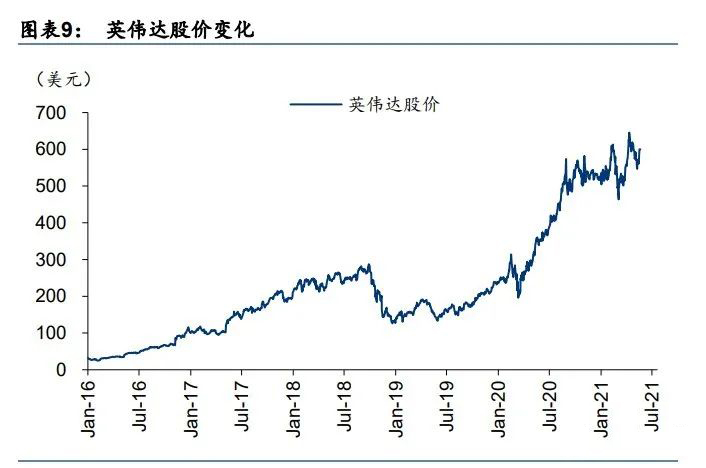

In the secondary markets of A-shares and US stocks, the market value of AI-related companies has continued to increase. Typical representatives of companies such as A-share traditional security leader Hikvision rely on AI technology to achieve product upgrades and industry breakthroughs; US stocks NVIDIA rely on GPU products to build AI chip computing power. The stock prices of the two companies have increased by about 4 times and 18 times respectively in the past five years

AI development in the next 10 years 1: computing power-AI reshapes the data center and automotive industry

The demand for computing power is mainly embodied in the form of AI chips, and the driving force comes from the most advanced AI algorithms. In the past ten years, OpenAI estimates that the global head AI model training computing power demand has doubled in 3 and 4 months, so the computing power required for the head training model has increased by up to 10 times each year. At the same time, the rapid increase in demand combined with Moore's Law has resulted in the price of computing power becoming more affordable.

At present, the data center and automotive fields have become the most important AI computing power development footholds, landing in the form of AI chips. Among them, there are only a handful of AI training chip manufacturers in the world. Related chips are mainly used in the cloud in the mode of servers, clusters, accelerator cards, etc., and will gradually appear on the edge; AI inference chips have a lower threshold than training, and some excellent ones. Start-up companies rely on the Fabless model to enter the market. Chip companies can provide dedicated artificial intelligence chips/IP and development tools: training chips are for customers in data centers, automobiles and other industries, and a large number of cloud companies design their own chips for internal use; inference chips are partially integrated in hardware terminals, such as mobile phones, cameras, and automobiles , Mining machines, etc., some of which are used to provide services in the cloud.

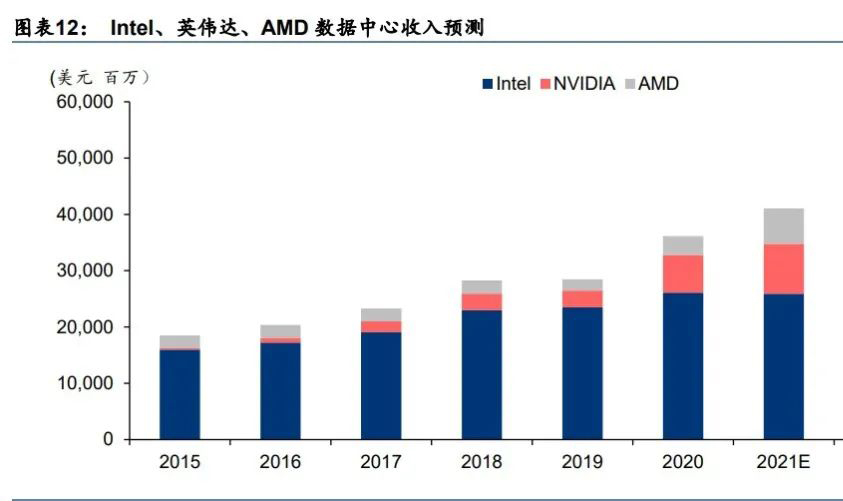

The processor chips used in servers and data centers continue to grow. At present, calculations still mainly rely on CPUs. As the demand for AI computing power increases, data center computing power shows a diversified trend. GPUs or ASICs mainly used for AI computing account for The ratio continues to improve. According to our calculations, the global server GPUs currently account for less than 20% of the market share of server-level processors, and the CAGR is expected to be about 25% in the next three years.

Facing market opportunities, global leading companies are rapidly supplementing their technical shortcomings through mergers and acquisitions. like:

1) Faced with the opportunity of heterogeneous computing, Intel has successively acquired companies such as Altera, Movdius, Mobileye, Barefoot, Habana Labs, etc. in the past few years, continuously improving the company's data center and computing capabilities in the automotive field.

2) In 2020, NVIDIA will acquire Mellanox and ARM (in progress). After announcing the acquisition, NVIDIA launched BlueField DPU (data processing unit) and CPU products for the data center market. DPU is positioned to offload tasks such as network, storage, and security on the CPU. Nvidia said that a BlueField-2 DPU can provide data center services equivalent to 125 CPU cores. The product similar to DPU is SmartNIC. In addition to NVIDIA, Intel, Broadcom, Xilinx, and Marvell all have a layout in the field.

3) AMD announced the acquisition of Xilinx in 2020, which is still in progress. Xilinx has the world's most advanced FPGA products, as well as adaptive SoC, accelerator and SmartNIC solutions, which effectively complement AMD's capabilities in the data center and edge areas.

Compared with the M&A wave of leading companies in overseas markets, a large number of startups in China have dedicated themselves to the design of AI chips in the data center and automotive fields, and have formed an evolutionary roadmap comparable to that of overseas companies.

In the current AI chip market, NVIDIA has a relatively high market share by virtue of its hardware advantages and software ecology. We judge: ①In terms of algorithms, the complexity of models is increasing; ②In terms of software, the use of AI frameworks is becoming more and more concentrated. Therefore, chips with large-scale model training capabilities will be more concentrated, and the types of chips supported by software tools will also be more concentrated. concentrated. Therefore, NVIDIA's advantages are difficult to shake in the short term.

But other domestic companies are also worthy of attention under the general trend of localization. In particular, these companies have greater opportunities in the inference market in areas such as edge computing centers, automobiles, and IoT. Inference chips customized for the industry may be the way to break the game. At present, a large number of customized reasoning chips have appeared in fields such as autonomous driving, cameras, and digital currency mining. The development of the industry in the future will be more clear. The development of the data center training market needs to rely on continuous research and development to narrow the gap.

AI development in the next 10 years 2: Algorithms-NLP, CV perception enhancement, breakthrough cognitive time is still unknown

The development of NLP and CV in the past few years has undergone algorithm breakthroughs, and has gone from traditional perceptual learning to the perceptual enhancement stage:

1) NLP: The algorithm breakthrough of NLP in the past ten years is one of the most important development directions in the AI ??field. In July 2020, OpenAI trained an AI model GPT-3 with 175 billion parameters based on a large amount of Internet text data, which can be applied to various NLP fields without further training. In 2021, Google released the Switch Transformer model, raising the model parameters to a scale of 1.6 trillion. Relying on the capabilities of large-scale models, the NLP field has been applied in a variety of new scenarios. Such as: web search, UI design, automatic programming, etc.

2) CV: In the past ten years, algorithms in the CV field have also been continuously upgraded, such as ResNet in 2015 and EfficientNet in 2019. In addition, a large number of algorithms are proposed for small sample inference scenes (YOLO), photo restoration (DeOldify) scenes, or 2D to 3D (PIFuHD) scenes. These algorithms have been rapidly applied in areas such as autonomous driving and media Internet.

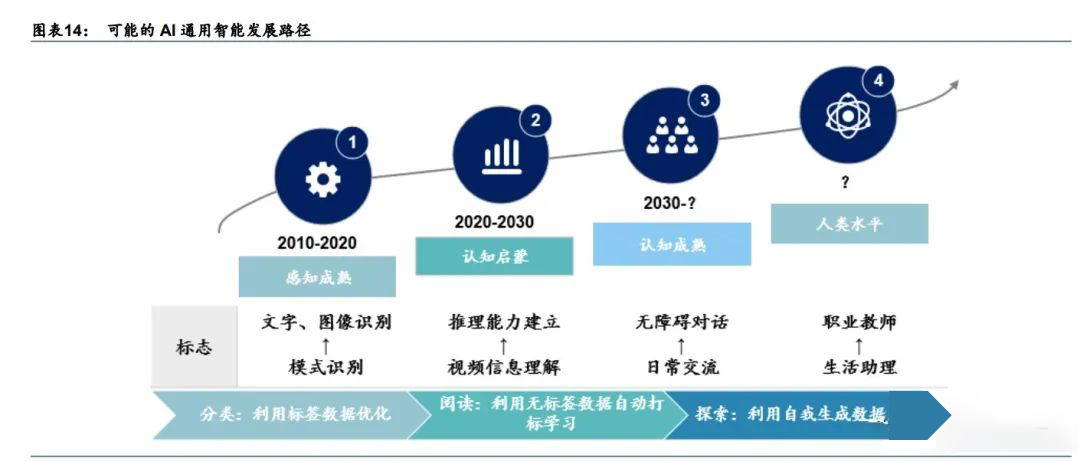

In a large number of scenarios, dedicated artificial intelligence can already meet most of the needs of human activities. However, after years of development, AI still remains at the perceptual level, and it is difficult to do deductive thinking like humans. We believe that in the next ten years, artificial intelligence will be integrated with brain science to develop general cognitive intelligence, which corresponds to applications such as human-machine multi-round dialogue and video understanding. However, the current implementation path is uncertain. Typical development ideas include:

1) Self-supervised learning that does not rely on a large amount of manually labeled data has become the new focus of learning methods. With the help of pre-training models, the learning results can be optimized by autonomously generating or enhancing data, relying on knowledge graphs and common sense relationships, and enhancing the learning ability under unlabeled data sets. Related cases include Google Bert, Facebook RoBERTa, Open AI's GPT-3, etc. Self-supervised learning is currently developing into the image field to achieve pixel-level target recognition. The purely supervised learning method training deep learning model phase is over.

2) Small samples, multi-modal learning, miniaturization of models. Migrating other training results, reusing knowledge structures in other fields, using a small number of sample training, and using multiple sources of information to expand learning capabilities are important development directions for AI. In addition, due to too many model parameters, FB, Tencent, Google, etc. are also accelerating the construction and improvement of model miniaturization capabilities. In TensorFlow, PyThorch, TensorRT and other frameworks, algorithms such as pruning and quantization are used to compress models to improve computing speed.

AI development in the next 10 years 3: Scenarios-multiple industries have high demand for CV, NLP and robots

AI has been very rich in the application of structured data and part of unstructured data (voice, text and image). Over the next ten years, with other innovations such as 5G, we believe that AI will rely on new algorithms, new computing power, and new sensor data to further challenge video and image scenarios and realize new business models. We believe that AI will have the most far-reaching impact in the automotive, medical and entertainment fields, and other industries also have various application scenarios.

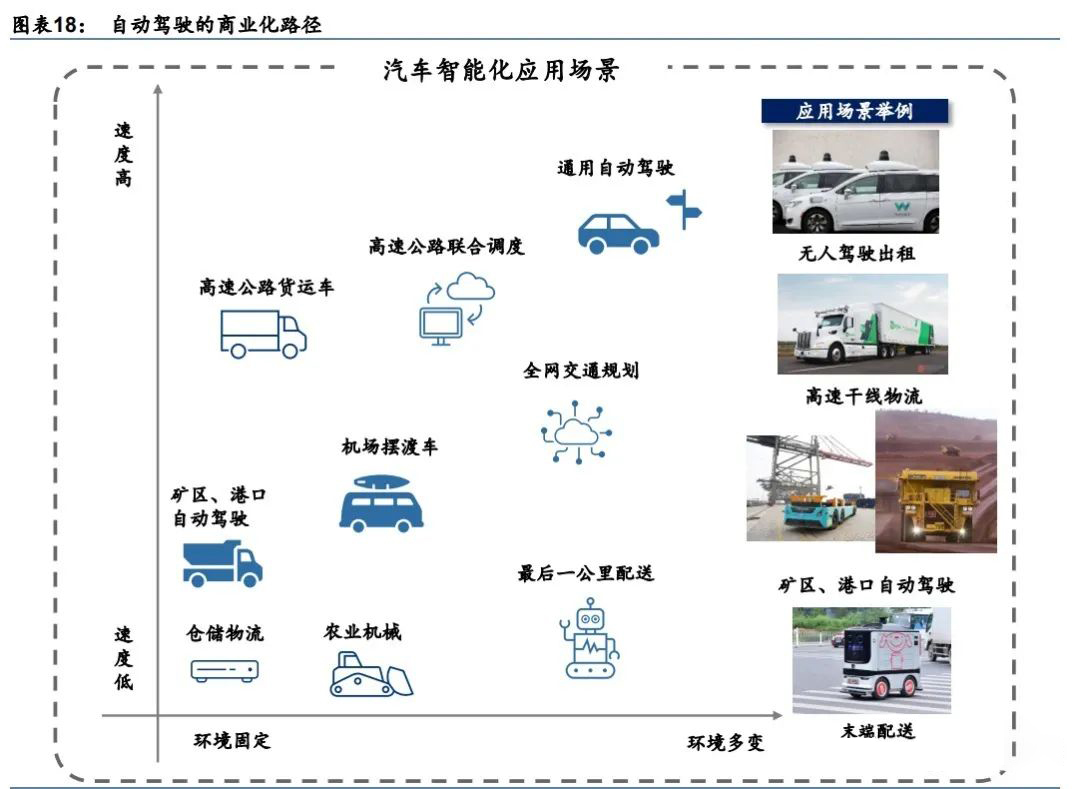

Cars-Autonomous driving results are optimized year by year, and slow-speed scenes are launched for commercial use

After years of development of autonomous driving, the industry's views continue to fluctuate. Before 2018, the industry was very optimistic about the development of autonomous driving. Events such as Google's establishment of Waymo, Uber's start of road testing, and Tesla's development of the Autopilot system have all attracted investors' attention. However, since 2018, the deployment of Waymo's autonomous driving has been slower than expected, and Uber has experienced fatal accidents with autonomous driving. In the face of general-purpose automatic driving in high-speed and complex scenes, a large number of long-tail scene problems are still to be solved, and it is difficult for L4 level automatic driving to be commercialized on a large scale. The focus on autonomous driving will increase again in 2020: In August, Baidu Apollo announced the launch of autonomous driving taxis. In October, Waymo announced that it would provide completely unmanned driving services. Tesla announced that it is about to complete the development of L5 autonomous driving. In 2021, a large number of leading companies will gather on the autonomous driving track, such as Apple (AAPL US), Amazon (acquisition of Zoox) (AMZN US), Xiaomi (1810 HK), Huawei (unlisted), Didi (unlisted) and so on. Although expectations are constantly changing, it is undeniable that road test results for autonomous driving are constantly improving. Although there is still a long way to go for autonomous driving, its development is more clearly driven by the leading companies.

Although there is still a distance to autopilot, it is difficult to clarify the specific commercial time, but it has been implemented in slow-speed scenarios, such as agricultural machinery, sweeping robots, express delivery and other scenarios, and there may be more slow-speed scenarios in the next ten years. Driving applications change people’s lives.

Medical care-a new decade of development where artificial intelligence enters the core link of diagnosis and treatment

We believe that the medical field is one of the main AI markets. In 2014, my country encouraged the development of AI medical devices, but the commercial use of products had problems with the implementation, resulting in slower-than-expected actual development. In 2018, IBM Waston significantly laid off its medical team and affected the development of the industry. One of the reasons for the layoffs is that the structured accumulation of data in the medical industry is small, and it is difficult for AI to obtain a better space for implementation. However, since the epidemic, the trend of AI medical treatment has been more widely accepted. There have been several breakthroughs in both theory and practice in the AI ??medical field, and three types of certificates for AI medical equipment will be issued one after another at the regulatory level starting in 2020. We judge that in the next ten years, AI is expected to be implemented in the form of algorithms, equipment and surgical robots in the fields of pharmacy, diagnosis, and surgery.

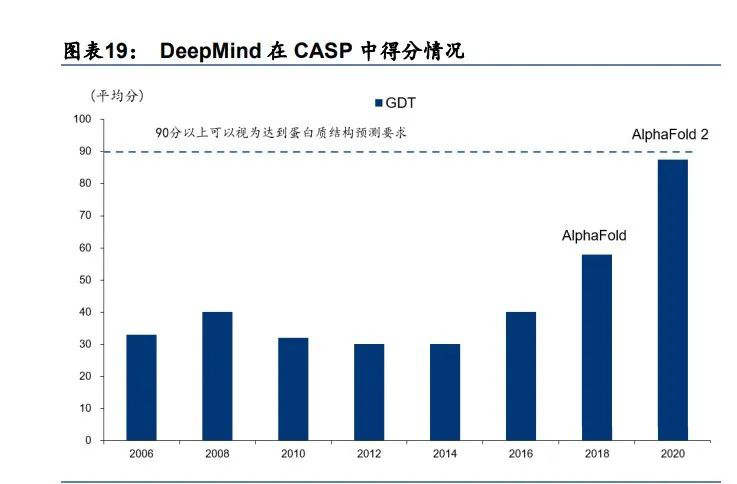

The most important application in the medical field is AI pharmaceuticals. In 2020, AI has solved the problem of protein structure prediction, which is a milestone problem in structural biology. In 2020, DeepMind ranked first in the authoritative protein structure prediction and evaluation competition (CASP) with the “AlphaFold 2.0” algorithm. Its main indicator GDT score reached 92.4 points, reaching laboratory level. In the past many years, pharmaceutical companies have extensively researched and promoted artificial intelligence technology, and it will be possible to use AI to build drug structures in the next ten years. AI can accelerate the drug development process by analyzing papers and clinical data. In the face of the new crown epidemic, AI has demonstrated impressive efficiency. In 2020, the British company BenevolentAI used AI to search massive literature to discover new crown drugs. The drug was later authorized by the FDA for emergency use. In the past two years, AI pharmaceuticals have been favored by the capital market. At present, the leading global AI pharmaceutical companies include Schrodinger (SDGR US), Recursion Pharmaceuticals (RXRX US), British BenevolentAI (unlisted), and China Jingtai Technology (unlisted).

The application of AI image recognition technology in the field of CT and MR film diagnosis has also been relatively mature, and it is expected to develop on a large scale in the next ten years. The products of companies including Keya Medical's Ark (unlisted), Lepu Medical (300003 CH), Tuxiang Medical (unlisted), United Imaging (unlisted) and other companies have been certified by the National Food and Drug Administration and can be commercialized in China .

The market size of surgical robotic therapy in the next ten years is also expected to continue to increase with the development of AI. According to the classification of the International Federation of Robotics (IFR), surgical robots are the most technically difficult robots and can be used for surgical image guidance and minimally invasive surgery. For example, there are mainly 7 similar companies in the orthopedic surgical robot industry. Among them, the companies that have obtained the registration certificate of orthopedic surgical robot medical devices are Israeli Mazor Robotics (acquired), French MEDTECH company (acquired) and American MAKO Surgical company (acquired) Acquisition); those who have not obtained the registration certificate for orthopedic surgical robot medical devices include Shanghai Fengsuan (unlisted), MicroPort Medical Robot (a subsidiary of MicroPort Medical Science Co., Ltd. (00853 HK)) and domestic neurosurgery robot medical care Bohuiweikang (unlisted) and Huake Precision (unlisted) with the device registration certificate. The above-mentioned companies have adopted robotic technology and realized the collaborative control of robotic arms based on surgical robot technology, forming a true surgical robot product. The emergence of new technologies has led orthopedic surgery into the era of robot intelligence assisted by the combination of image navigation and robotics technology, which has had a subversive impact on hospital diagnosis and treatment methods and the competitive landscape of medical equipment.

Others-AI is full of imagination in various industries

1) The mobile Internet field uses deep learning to achieve better development in the recommendation system and other fields. In the future, through the implementation of perceptual intelligence, more humane intelligent customer service will appear in the mobile Internet field, and chat robots will appear to accompany humans.

2) In the field of security, simple video analysis such as moving target recognition, face recognition and other applications have been very mature, but the grasp of intent, etc. is still not mature enough. In the future, with the development of CV technology, the understanding of video will be improved to a higher level. Through the video, the target trajectory can be predicted and early warning can be given.

3) In the field of smart home, smart door locks with fingerprint recognition and smart speakers with simple conversation capabilities have been widely used. Similar to chat robots, smart home assistants are still in their early stages of development.

4) In the retail field, unmanned retail has been promoted in some areas. Users can open the shelves to pick up items through self-service scan codes and other modes. The shelves use cameras and other sensors to identify the products and automatically settle. Some shopping malls have already installed shopping guide robots, and in the future, more intelligent shopping guide robots will be smarter, enabling more in-depth products instead of store shopping guides.

5) In the financial sector, the existing AI has mature applications in areas such as customer qualification screening, and CV applications are concentrated in areas such as remote account opening. The current remote dialogue services are generally connected to customer service specialists, and robo-advisors may appear in the future.

Meta universe-AI connects the virtual world and the real world

The automotive and medical industries discussed above are only subdivisions under the concept of meta universe. We believe that AI technology will become an accelerator for the arrival of the Metaverse era. The game "Minecraft" has implanted the concept of virtual parallel world into the hearts of the public, and the concept of meta-universe may be a profound trend in the development of the industry.

In a narrow sense, the establishment of the meta-universe requires 3D reproduction of real life content. The traditional 3D production process requires basic modeling, texture mapping, lighting rendering and other steps, and it is becoming more and more complicated. Nvidia will release the Omniverse 3D simulation and collaboration platform in 2020, which can simulate the real world realistically, improve the flexibility and scalability of industry workflows, and realize the digital twin of the virtual and real world. In the past two years, more than 400 companies have evaluated Omniverse. Nvidia's Omniverse ecosystem continues to expand, linking industry-leading applications from various software companies, and striving to create an open source standard and interoperable Metaverse.

Broadly speaking, the construction of Metaverse helps the entire industry to digitize. A large number of services that rely on humans can achieve digital landing in Metaverse. And the most complicated one is the long tail scene in each scene. Traditional AI pursues the sophistication of algorithms and models, but it cannot cover the tail scene. However, the industry has undergone profound changes in the past year. The large-scale algorithm + violent computing power model has caused the model to cover long-tail scenarios. The open AI platform also allows more and more traditional industry engineers to participate in the development of AI models. Therefore, the rise of the meta-universe concept is also an inevitable result of the development of AI.

AI development in the next 10 years 4: Data-Legislation has been implemented, and the scale of commercial data transactions is still unknown

After deep learning, data has become one of the most important means of production, and a series of issues such as infringement and big data acquaintances that accompany data have also received attention. The European Union proposed in 2016 to implement the General Data Protection Regulations (GDPR) in 2018. This bill has aroused global awareness of data protection and personal information protection. China has implemented the "Cyber ??Security Law" in June 2017, implemented the "GB/T 35273 Information Security Technology-Personal Information Security Specification" in May 2018 and implemented the new version in November 2020. The U.S. federal government established the U.S. "Clarification of Extraterritorial Legal Use of Data Act" (the Cloud Act), and each state has established about 30 laws on Internet data since 2018.

Under legal constraints, barriers to data exchange have increased. In July 2020, the European Union declared the "Privacy Shield" plan invalid based on the GDPR, which complicates the flow of European data to the United States. In the same year, the U.S. government banned data sharing between TikTok and Chinese companies, and my country required apps such as Zoom to carry data in China's data centers. In the context of trade frictions, cross-border data sharing has become complicated, and the development of AI companies may be regionalized.

Data opening is also facing changes on the technical side. The world's leading algorithm company, such as OpenAI, launched the GPT-3 algorithm, but did not open its model, but instead used it in a commercial way. In the open source community, open source projects imitating GPT-3 such as GPT-Neo, Connor Leahy, etc. have appeared. Due to the open source ecology of algorithms, the value of data is highlighted. The leading algorithms currently rely on large databases. For example, GPT-3 and Switch Transformer train their models with reference to almost all texts on the Internet, with parameters above 100 billion. Therefore, small, non-public data sets contribute little to the value of AI's technological breakthroughs. In contrast, industry-specific data is more precious.

The opening of data in the future may start with public data. In March 2020, the Central Committee of the Communist Party of China and the State Council issued the "Opinions on Building a More Complete System and Mechanism for the Market-based Allocation of Factors", which clearly stated that "promote the open sharing of government data. However, the openness of enterprise data may still require long-term continuous attempts. It is difficult to form a unified model.

2. Blockchain 2030: From digital currency to the underlying technology of financial infrastructure

Blockchain development review

In November 2008, the author under the pseudonym Satoshi Nakamoto published "Bitcoin: A Peer-to-Peer Electronic Cash System" and proposed the concept of Bitcoin for the first time. In the past ten years, Bitcoin, Ethereum, and Ripple have appeared in the cryptocurrency market one after another. Industrial chains such as mining machines, miners, and mining pools have gradually taken shape, and the scale of transactions has continued to expand. Later, in order to not only maintain the anonymity and decentralization of blockchain technology, but also overcome the problem of large volatility of cryptocurrency relative to legal currency, stable currency came into being. In 2019, Facebook launched Libra in combination with stablecoin technology and its huge user base, which stimulated countries to accelerate the exploration of central bank digital currencies. In the next ten years, the application of blockchain technology is not limited to the encrypted asset industry. On the one hand, it will use Ethereum as an important asset carrier to derive more ecology; on the other hand, it will deepen the platform's development while improving the financial infrastructure. The construction and expansion of application scenarios will eventually form an ecosystem of all things inter-chaining.

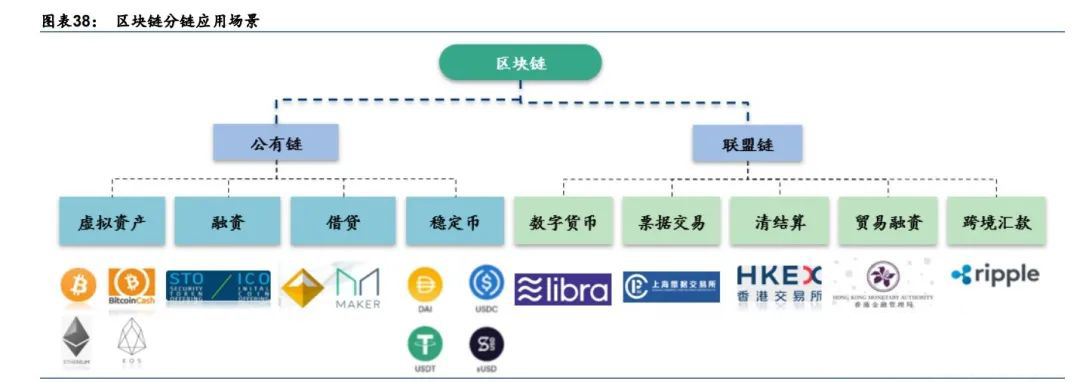

Blockchain can be divided into public chains led by open source communities and consortium chains led by large IT or financial companies. (1) Public chain applications, represented by Bitcoin, have been fully rolled out and are completely decentralized. Anyone can access without authorization. Nodes can enter and exit the network freely. Typical representatives are Bitcoin and Ethereum. However, due to the complexity of the public chain model, the small transaction carrying scale, and the large delay, it is generally suitable for application scenarios such as virtual currency and Internet finance. (2) The consortium chain is expected to realize the scene landing. The alliance chain requires specific nodes to participate and trade, which can achieve partial decentralization. Because the entire chain is small in scale, easy to control, efficient, and large in carrying transactions, it is generally suitable for inter-bank transfers, stock exchange clearing and settlement, corporate traceability, monitoring and auditing, etc. Typical representatives include R3 Blockchain Alliance, Hyperledger, etc., which are currently the preferred type of combination of blockchain in the fields of finance, public services, and supply chains.

Up to now, blockchain technology is not limited to virtual assets. It has begun to play an active role in the fields of clearing and settlement, payment, electronic invoices, supply chain finance, electronic invoices, and trade finance.

Digital assets have become an asset class that cannot be ignored

Digital assets represented by Bitcoin have maintained significant growth. The emergence of Bitcoin in 2009 brought blockchain technology to the public eye. With the active market of encrypted assets, Ethereum, Dogecoin, Ripple, etc. have emerged one after another, which simultaneously stimulated the gradual development of industrial chains such as mining machines, miners, and mining pools. form.

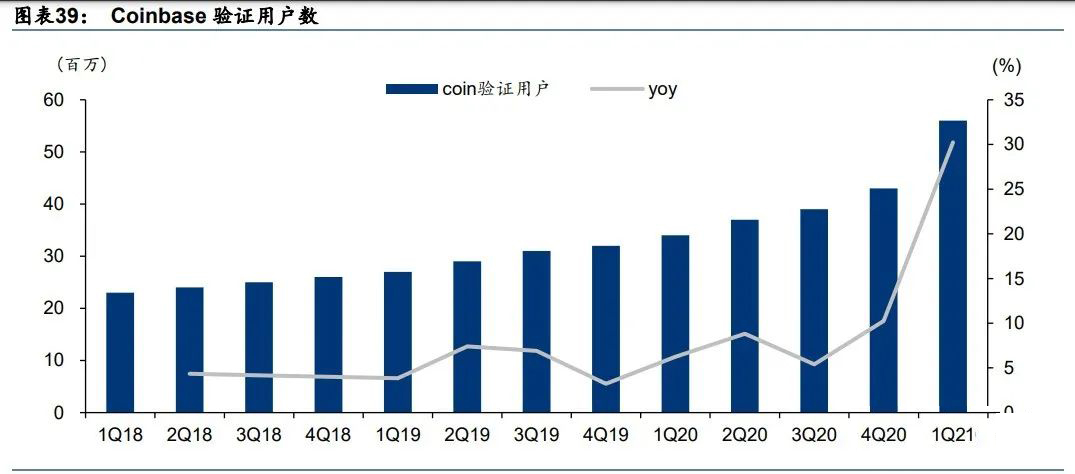

Despite the recent decline in the price of Bitcoin, according to the statistics of OKEx, its market value accounts for 10% of the market value of gold, and it has become an important asset class in the world. According to Coinmarketcap data, the total market value of cryptocurrencies in 1Q21 has exceeded US$2 trillion. At the same time, the number of users of Coinbase, the world's leading cryptocurrency exchange, is also increasing. The number of accounts has increased from 500,000 in 2013 to approximately 56 million in 1Q21, with revenue of US$1.8 billion in 1Q21, and its growth rate has significantly exceeded the market. expected.

Traditional investors actively invest in Bitcoin assets

The investment in digital assets is not declining, and the trading interface is open to lower the investment threshold. From the perspective of blockchain investment and financing, digital currency is still an important investment area for capital. In recent years, a number of new financial products and channels for digital assets have emerged, providing investors with convenience and compliance for entering the market. For example, the first Bitcoin Trust Fund (GBTC) in the market established by Grayscale in 2013 serves investors through a compliant fund operation method. The secondary market transactions are not restricted, which reduces the threshold for investors and eases Investors are worried about the storage and security of encrypted assets. At the same time, PayPal (payment software), Robinhood (stock trading software), etc. also attract investors to invest in digital assets by cooperating with crypto asset brokers to open trading interfaces.

Central banks of various countries are actively developing digital currencies, and China takes the lead in trial operation

The three-legged global digital currency pattern has taken shape. Among various encrypted assets, stablecoins retain the advantages of a simple cryptocurrency settlement process and strong anonymity, and avoid the volatility risk of cryptocurrencies, and their prices remain relatively stable. We believe that stablecoins will become the main value scale and mainstream payment tool in the crypto asset industry.

The digital currency process of the People's Bank of China is in a leading position in the world. The discussion and framework establishment of my country's central bank digital currency theory has begun around 2014, and related technologies have been improved in 2016. In 2019, it has entered the stage of accelerated implementation. On January 10, 2020, the official official account of the People's Bank of China stated that it has basically completed the top-level design, standard formulation, function research and development, and joint debugging and testing of legal digital currency. Since April, my country's DC/EP has successively conducted internal closed pilot tests in Shenzhen, Suzhou, Xiongan, Chengdu and future Winter Olympic scenes. With the rapid advancement of central bank digital currencies, my country is expected to become the main economy that first issues central bank digital currencies.

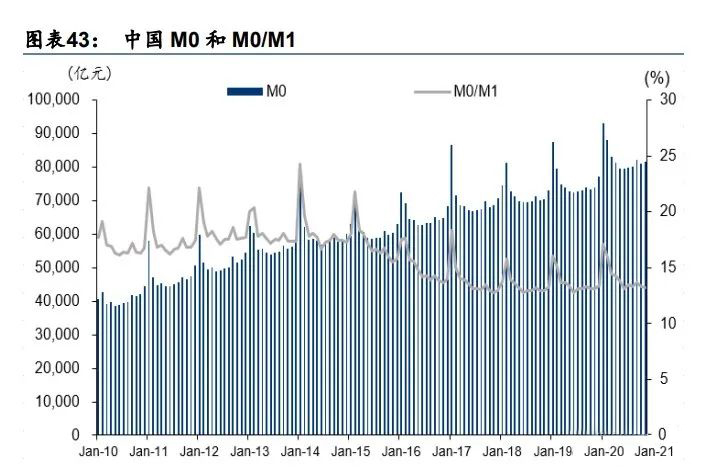

The emergence of digital currency is more adaptable to the development of a cashless society, reshaping the payment pattern. For a long time, the currency of the central bank circulated in the public market in the form of physical cash. With the popularity of smartphones and the rise of third-party payments, the epidemic also places more demands on contactless services, and the utilization rate of physical cash continues to decrease. According to Wind data, the ratio of M0/M1 in China has dropped from 18% in 2013 to 13% in 2020, and M0/M1 in some Nordic countries has even dropped below 5%. Since CBDC has a higher credit rating than commercial banks and third-party payment institutions, and taking into account the costs of physical cash issuance, transportation, circulation, and management, we believe that CBDC may break the industry monopoly in the payment field and reshape the payment competition landscape.

Blockchain development in the next 10 years 1: Ethereum has become an important asset carrier, and the product matrix is ??becoming more abundant

Ethereum is becoming an important asset carrier, and the market value of stablecoins and Bitcoin on the chain continues to increase. From the launch of Ethereum in 2015 to the launch of Ethereum 2.0 in 2020, after 5 years of development, Ethereum has become one of the most important blockchain infrastructures. Due to the security, convenience and rich DApp ecology of the Ethereum network, users began to transfer their assets to Ethereum, such as using Ethereum-based stablecoins and collateralizing Bitcoin to the Ethereum network in exchange for corresponding ERC-20 bits Currency etc. In terms of scale, the current total market value of Ethereum is approximately US$300 billion, which has increased by more than 5,000 times compared with 2016, and has become a carrier of many important assets. From the perspective of application types, Ethereum has gradually transitioned from its original use in gambling and high-risk fields to the fields of finance, trading, and security, and its ecology tends to be more valuable.

DeFi ecological growth, the formation of traditional financial forms represented by currency, banking, insurance, etc. Centralized finance (DeFi) refers to the use of decentralized infrastructure (such as public chains and smart contracts) to build financial services such as lending and transactions. It has the characteristics of centralization, no permission, openness, and both lower fees and higher safety. Compared with traditional finance relying on intermediaries, DeFi automatically provides users with various services through blockchain protocols and DApps, which greatly provides convenience. At present, the DeFi ecosystem has covered a variety of traditional financial forms such as currency, banking, insurance, payment, and asset management, and the lock-up scale exceeds US$10 billion.

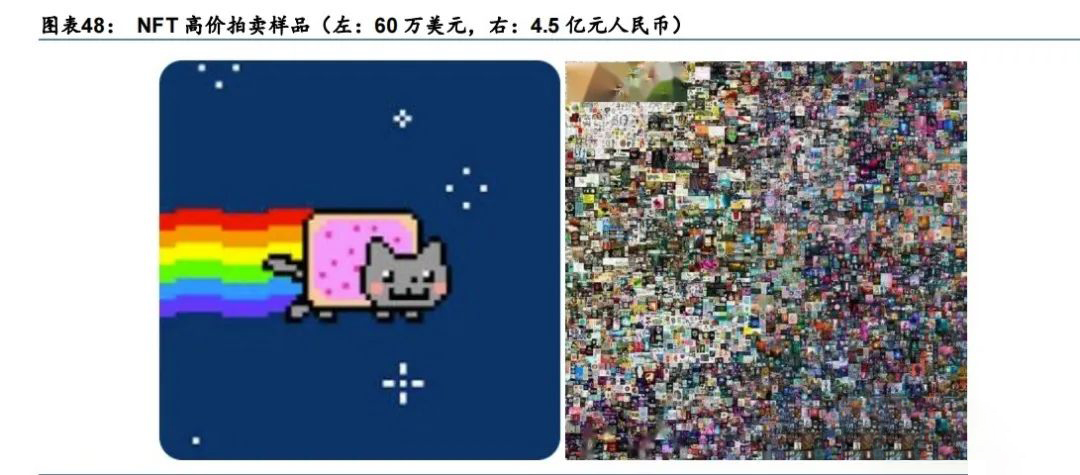

The emerging concept of the digital circle NFT enters the field of vision, or will play a role in the field of certification. Since NFT first entered the public eye in 2017 in the form of Ethercats, nowadays, high-performance blockchain and layer 2 solutions continue to emerge, and various expansion solutions make high-throughput DApps a reality. Collectors and artists look at Back to the field of NFT again, novel works that have been uniquely certified by NFT have been auctioned at unexpectedly high prices many times. We believe that although the use of NFT to represent real-world assets is still in the early stage of exploration, it has huge application potential. In the future, physical assets can be represented in the form of tokens in real estate, certificates, documents and other fields to achieve information transparency and on-chain Automatically execute transactions on.

Blockchain development in the next 10 years 2: Blockchain is expected to become the core technology of the next-generation financial infrastructure

Blockchain will be used as a multi-business underlying technology to empower the financial field. At present, blockchain as the underlying technology is widely used in encrypted digital assets, central bank digital currency, payment and settlement systems, securities trading platforms, trade financing platforms, etc. my country pointed out in the 14th Five-Year Plan that in the future, the development of blockchain will focus on alliance chains to develop blockchain service platforms and applications in financial technology, supply chain management, government services and other fields. This means: (1) Blockchain participants are more abundant, mainly through the construction of platform layers led by companies such as Tencent, Alibaba, and Funchain Technology to provide productized services such as smart contracts, information security, data services, and government For the construction of blockchain infrastructure in the leading financial and government fields, the two will accelerate the landing of the alliance chain on the basis of the public chain; (2) In the future, there will be more financial scenarios to achieve the chain, with multi-party sharing and high frequency Elements characterized by repetition will use blockchain technology more frequently:

1) Realize multi-party sharing. The blockchain based on encryption technology will play a role in the realization of information sharing. In financial scenarios such as cross-border payment, cross-border trade financing, supply chain finance, and asset securitization (ABS), mutual cooperation between independent financial institutions is often required. Blockchain can significantly reduce the communication cost of all parties.

2) Suitable for high frequency repetition. The smart contract of the blockchain can realize business automation. Therefore, it is very suitable for high-frequency repetitive businesses such as electronic payment, post-transaction clearing, and regulatory risk control.

3. Commercial Aerospace 2030: From Satellite Internet to Martian Immigration

Commercial rocket development review: SpaceX began to change the launch market pattern

We believe that SpaceX has reshaped the global rocket launch industry with technologies such as rocket recovery. Previously, rocket launches have been mainly carried out by the government for one-off large-scale projects, such as the establishment of a space station, human landing on the moon, Mars exploration, and the construction of the Beidou system. It is difficult to form commercial operations. From the perspective of rocket launch data, global government rocket launch projects have fallen sharply since 2013.

SpaceX has truly brought a subversion to the traditional aerospace industry. SpaceX has promoted technological breakthroughs. Through the vertical integration of the industry chain, it has mastered key technologies such as rocket recovery technology and multiple stars with one arrow. At the same time, the company has selected a large number of consumer electronics industry chains to make rocket core components (such as engines, turbo pumps, electrical equipment and motherboards). , Flight computers, solar panels, etc.) to replace aerospace-grade equipment, and optimize the rocket assembly process, so as to constantly refresh the launch cost. At the same time, Space X uses projects such as Starlink as pilots to greatly increase the frequency of rocket launches, and further amortize launch costs through scale effects, which has brought about a continuous drop in launch prices. The fall in the price of commercial rockets will bring subversion of a series of industries, such as communications, travel, transportation, and deep space exploration.

The development of SpaceX allows investors to see the direction of investment. In 2019, the scale of investment in the primary market exceeded US$4 billion, giving an optimistic outlook on the development of the aerospace market. Under the positive cycle of technology and capital, a large number of rocket companies have also continuously improved their rocket capabilities in the fields of engines, propellants, and boosters, and conducted a large number of tests to obtain good results.

SpaceX is unlikely to be listed in the short-term, but by the beginning of 2021, the valuation in the primary market has reached 74 billion U.S. dollars. Among the primary market companies, Rocket Lab is one of SpaceX's main competitors. Rocket Lab was established in 2006, and the company is expected to be listed on NASDAQ in 2Q21. Rocket Lab has successfully launched 18 Electron rockets and is developing Neutron rockets. The company achieved its first launch in 2017, serving commercial satellites and government agencies. In addition, American startup companies also include Astra, Relativity and so on.

Commercial aerospace development in the next 10 years 1: Satellite Internet reshapes the communications industry

Due to the sharp drop in the price of rockets, satellite Internet replaces large-area underground optical fiber laying and solar energy instead of electric energy through satellite links, making it possible for universal network services around the world. We believe that the existing earth network is relatively mature, and the value of satellite internet will be further highlighted in the future Martian immigration process.

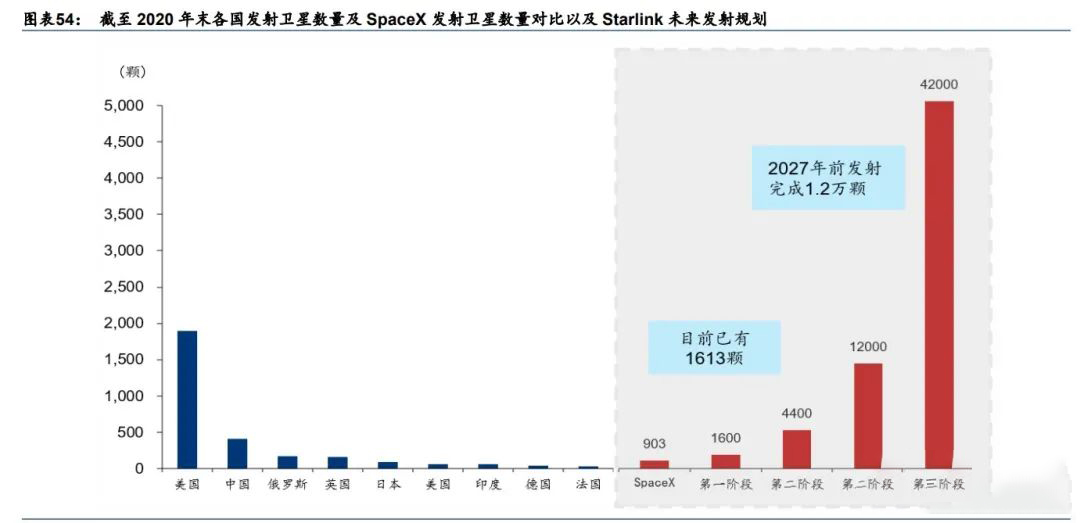

SpaceX CEO Elon Musk first proposed the "Starlink" plan in 2015. The plan is divided into two phases and three phases. It plans to launch a total of 12,000 satellites to orbit around the earth between 550 and 1,325 kilometers to form a broadband satellite communication network that can cover the world. The total scale of satellites will be expanded to 42,000 (capacity may continue to be expanded in the future). SpaceX began satellite launches in May 2019. As of March 18, 2020, it has successfully launched 6 times with a total of 360 satellites in orbit. From the perspective of the number of satellites, it has become one of the world's largest satellite operators. At the current rate of launching "60 satellites in one arrow" every 2 to 3 weeks, we expect SpaceX to have about 1,600 satellites by the end of 2020, which is more than the number of satellites in any country as of 2020.

SpaceX launched the Starlink project in 2015, hoping to launch 42,000 to 54,000 satellites in the long-term, and use satellites as base stations to form a global Sky Internet. Among them, the first batch of 12,000 satellites was launched in three phases:

1) Phase 1: Launch about 1,600 satellites. The official satellite launch will begin in May 2019. The LEO orbital target located 550 kilometers above the ground provides basic coverage of global networking;

2) Phase 2: Launch about 2,814 satellites, which will be launched soon, and the goal is to complete the global network. The previously planned altitude was 1100-1300 kilometers. In April 2021, it was approved by the FCC to be lowered to the LEO orbit located 540-570 kilometers above the ground, which is basically the same as Phase One;

3) Phase 3: It is estimated that by 2027, there will be about 7,518 satellites remaining after launch, with an orbital height of 350 kilometers, and the goal is to provide global high-speed networking services.

The first two phases of the satellite use the Ka/Ku band (10~30GHz), and the third phase of the satellite uses the Q/V band (37.5x-53.0GHz). Due to the continuous improvement of rocket capabilities, the technology of multiple satellites with one rocket has been widely used in the field of satellite launches, with a single launch of up to 60 satellites. SpaceX has recently been advancing in accordance with the launch mode of "60 stars per arrow" every two weeks. As of May 9, 2021, SpaceX has launched a total of 1,613 satellites through 27 special networking missions. We expect the company to achieve global interconnection after the next launch. Phase 1 is basically completed and Phase 2 starts. In the next few years, the number of satellites launched each year may be more than 1,000. We believe that SpaceX currently has more satellites than any country, becoming the world's largest satellite operating company.

The Starlink project overturned the satellite Internet industry. Due to the high price of existing satellite communications, the scale is less than 1% of terrestrial communications, mainly serving specific scenarios. Starting in October 2020, SpaceX started the public test of Starlink. By February 2021, there were more than 10,000 users in the United States and other countries; on May 6, 2021, more than 500,000 people had prepaid a $99 deposit to book online services. The current monthly fee is US$99, and the download speed is 50-150MB/s. On April 15, 2021, SpaceX stated that “it will be fully mobile in 2021”, serving scenes such as cars, ships, and airplanes; it is also said that Starlink is developing portable terminals with the US military to support the military’s mobile communication scenarios. . Currently, Starlink's equipment terminal sells for 499 US dollars, but the cost is showing a downward trend. The early cost is as high as 3000 US dollars. In December 2020, the cost is about 2000 US dollars. In April 2021, the cost has dropped to 1500 US dollars.

In the long run, Starlink will provide a mobile communication network for the world, with a communication capacity of 1Gbps, a delay of less than 25ms, and a user-segment terminal unit price will be controlled within US$200. SpaceX is also looking forward to obtaining 25 million Starlink users in the long run, bringing about 30 billion U.S. dollars in annual revenue to support the development of SpaceX. In the long run, once a network needs to be established on Mars, satellite Internet will become the best choice for network construction due to its low power consumption and low deployment cost.

The Starlink project disrupted the communications industry as well as the satellite manufacturing industry. The aerospace industry has always regarded the government as the most important customer, and price is not the first consideration. Therefore, the supply and demand pattern of the industry is solidified and the pace of business is slow. SpaceX has reshaped the satellite market model and structure, pushing satellites from the era of customization to the era of industrialization and marketization.

Driven by SpaceX’s Starlink, there has been an upsurge in the construction of satellite Internet around the world. On April 20, 2020, my country included satellite Internet into the policy encouragement scope of “new infrastructure”; while global technology companies such as Google (GOOGL US), Amazon (AMZN US), Facebook (FB US), Apple (AAPL US), Huawei , Samsung, and Boeing (BA US) have also joined the construction of satellite Internet. In addition, existing companies in the industry such as Viasat (VSAT US), OneWeb (unlisted), Hughes Network Systems (unlisted), and Boeing are considering forming alliances to compete with SpaceX.

Application 1: Broadband network global coverage, target future Mars network construction

By the end of 2020, more than 30% of the world's population still has no access to mobile networks, and more than 20% of the population in areas covered by mobile networks still do not use mobile Internet services. In addition, the existing network technology facilities are built around human settlements. Most of the world's 71% of the ocean area, 7% of the forest area, and 6% of the desert area are not covered by the existing communication network. In terms of coverage height, the existing network only covers 100 meters above the ground, and there is no coverage capability at high altitude. Satellite Internet covers the whole world and is an effective supplement to existing communication technology. It can not only provide network connection services for remote areas or the aviation industry, but also provide special services such as forest fire prevention and remote rescue for special scenarios. This advantage may not be obvious on the earth, but once immigrate to other planets in the future, the rapid construction of satellite Internet is very necessary.

Application 2: Bright prospects for military use, the US military continues to deepen cooperation with satellite Internet companies

Satellite Internet, with its advantages of low latency, high throughput, and wide coverage, will help realize data interaction across multi-dimensional battlefields such as land, sea, air, space, network, and electricity, and enhance multi-domain combat capabilities. Joint operations command, battlefield situation awareness, unmanned system operations, and ballistic missile defense are applied in multiple fields. In 2018, the U.S. Air Force took the lead in signing a $28 million service contract with Space X, focusing on verifying how to integrate the satellite Internet provided by Starlink into the military data network to enhance its ability to implement multi-domain operations; May 2020 , The US Army and SpaceX signed a three-year cooperative research and development agreement, focusing on verifying how the Starlink satellite Internet system integrates software and hardware with the Army's mobile combat forces. If progress goes well before 2024, the US Army will intend to purchase about billions of dollars in satellite Internet services with Space X.

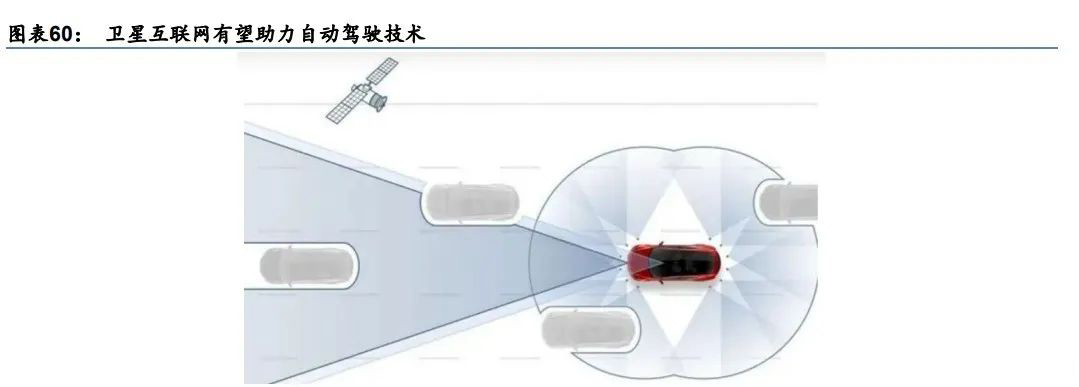

Application 3: Wide coverage + high flexibility + low-latency data transmission capabilities, helping the Internet of Vehicles to become reality

The prerequisite for the realization of autonomous driving is the realization of stable and high-speed data transmission between the car and the cloud. The satellite Internet provides the possibility to realize this technology. As a natural global network, satellite Internet has a global wide-area coverage capability, which can provide continuous and stable network connections for autonomous driving services and improve the safety and reliability of autonomous driving. In addition, compared with the fixed signal bandwidth of ground base stations in local areas, satellite communications can provide services with a certain capacity flexibility, ensuring that stable access services can still be provided in congested areas. After Musk, other automakers are also actively exploring the application of satellite Internet in the Internet of Vehicles, including Weilai Automobile (0305 ??HK), Weimar Automobile (unlisted), Xiaopeng Automobile (XPEV US) and so on.

Commercial aerospace development in the next 10 years 2: Intercontinental spacecraft and space travel reshape aviation and tourism

According to Musk, with the commercial maturity of SpaceX rocket BFR, the rocket can be used for intercontinental transportation. Intercontinental transportation dropped from the 10-hour level to less than one hour, greatly facilitating the global transportation market.

Virgin Galactic and other companies in the United States are promoting space travel services, as well as microgravity experimental applications and astronaut training applications. The single price is at the level of 250,000 US dollars. At present, about 600 people have subscribed to the service. Nearly 10,000 people are willing to experience related products. The company is still testing its spacecraft and has completed 4 tests. Five aircraft will be put into service in 2023.

Commercial aerospace development in the next 10 years 3: Business models such as moon bases and Martian immigration are expected to become a reality

As the Earth’s climate problems become more serious, humans urgently need to explore extraterrestrial planets to deal with various uncertainties. According to Musk’s judgment, SpaceX may complete its first cargo to Mars as early as 2022 (previously estimated to complete the manufacture of propellers and spacecraft in 2025), and realize the ambition of a manned spacecraft to land on Mars in 2024. It is expected to go to Mars in the middle of this century. One million people have emigrated. This timetable is supported by NASA, and NASA also believes that the first astronauts will go to Mars in 2024. Due to the orbit, the optimal time to land on Mars occurs once every two years. SpaceX and others are aiming for the 2024 plan and strive to land on Mars as soon as possible. Prior to this ambition, with breakthroughs in space technology, we believe that the following commercial scenarios are expected to land. At the same time, American and Chinese scientists are discussing the possibility of establishing a space base on the moon. The space base can be used as a test environment for astronauts to prepare for migration to Mars.

China's 14th Five-Year Plan promotes accelerated industry development

The development of the global aerospace market is currently dominated by China and the United States. my country has a relatively complete aerospace system industry chain and is internationally competitive. However, the development of SpaceX has also promoted the progress of my country's aerospace industry, and promoted my country's thinking about how to move from an aerospace power to a space power.

1) In terms of satellite Internet, my country’s early satellite Internet construction plans include: Aerospace Science and Technology Hongyan, Aerospace Science and Industry Hongyun, China Electronics Technology Xingyun, Galaxy Space Galaxy and other constellation projects. Among them, there are more than 10 low-orbit satellite projects with more than 30 networks, and the planned total number of satellite launches is close to 2,000. After the “new infrastructure” was put forward, my country's satellite Internet thinking gradually became clear. On April 28, 2021, the State-owned Assets Supervision and Administration Commission announced the establishment of China Satellite Network Group Co., Ltd. (Xingwang Company) with Xiong'an as its headquarters. In addition, the construction of satellite Internet is related to the future global interconnection services and is also one of the future development directions of 6G.

2) In terms of rocket launches, the number of launches in my country is expected to exceed 40 for the first time in 2021, serving space station orbit construction missions, Tianwen-1 Mars landing patrol and detection, civil space infrastructure business satellite launches, and Beidou global satellite navigation system applications.

3) With regard to the construction of the Chinese space station, the core module of my country’s space station will be successfully launched in 2021. Around 2022, the construction of the space station structures such as Tianhe Core Module, Wentian Experimental Module I and Mengtian Experimental Module II will be completed and operations will begin. The society is open to cooperation.

4) In terms of deep space exploration, my country's Tianwen-1 will land on Mars in 2021. Around 2030, my country will also plan to implement Mars sampling and return, asteroid exploration, and exploration of the Jupiter system, conduct research on key technologies, and promote deep space exploration projects. Implement. my country's Chang'e 6-8 will conduct lunar surface tests to demonstrate the possibility of lunar research stations.

5) In addition, the development of my country's Beidou and remote sensing systems will also be further deepened.

In the past few years, a number of outstanding companies have emerged in my country in the commercial aerospace field. Among them, the development of my country's commercial rocket-related companies is progressing smoothly, which is expected to promote the rapid growth of the industry.

Back